Dodatkowe Informacje I Objaśnienia Dla Jednostki Małej

Dodatkowe Informacje i Objaśnienia dla Jednostki Małej (often abbreviated as DII) are a crucial part of the financial statements of small entities in Poland. They supplement the balance sheet, profit and loss account, and cash flow statement (if prepared). Think of them as the notes accompanying the financial statements, providing essential context and clarity.

What's their main purpose? The DII explain and justify the figures presented in the primary financial statements. They provide information that is necessary for a fair and understandable view of the entity's financial situation and performance.

So, who actually needs to prepare DII? Polish accounting regulations specify which entities are considered "small." Generally, this applies to companies that meet at least two of the following criteria in the year preceding the financial year:

Must Read

- Average annual employment of less than 50 employees.

- Total assets at the end of the financial year less than EUR 4,000,000.

- Net turnover from sales of goods, products, and financial operations less than EUR 8,000,000.

Now, let's break down what needs to be included in the DII. While the specific requirements may vary slightly, core elements are always present. Here's a simplified look:

- General Information About the Entity: This includes the name, registered address, legal form, registration number (KRS), main business activities (PKD), and the length of the reporting period. It's the basic identity of the company.

- Accounting Policies Applied: This section details the accounting principles used to prepare the financial statements. For instance, how is depreciation calculated? Which valuation methods are used for inventory? Consistency is key, so this is important.

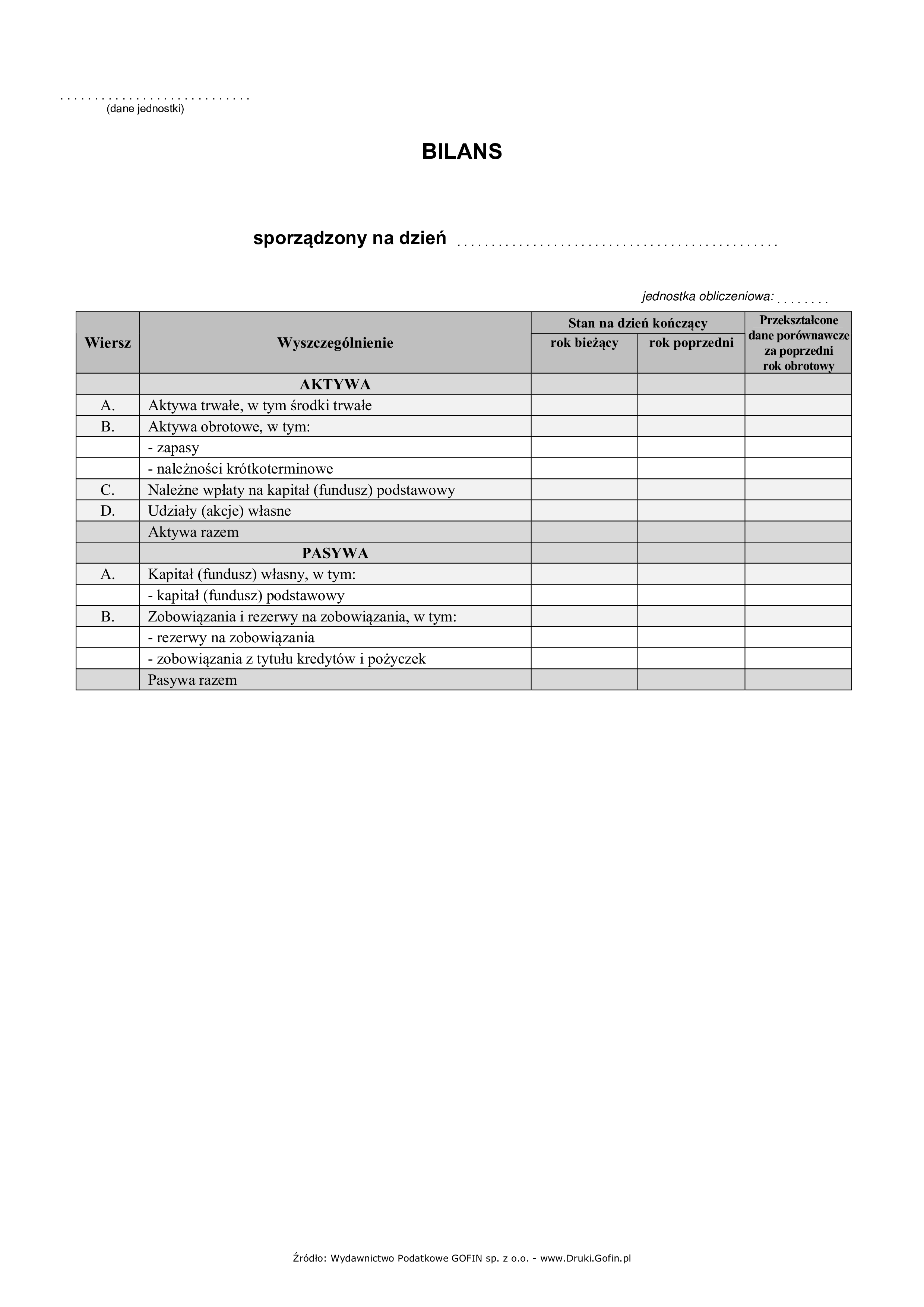

- Detailed Information on Selected Items: Here, you provide breakdowns of specific balance sheet and income statement items. For example, you might explain the composition of fixed assets or the nature of revenue.

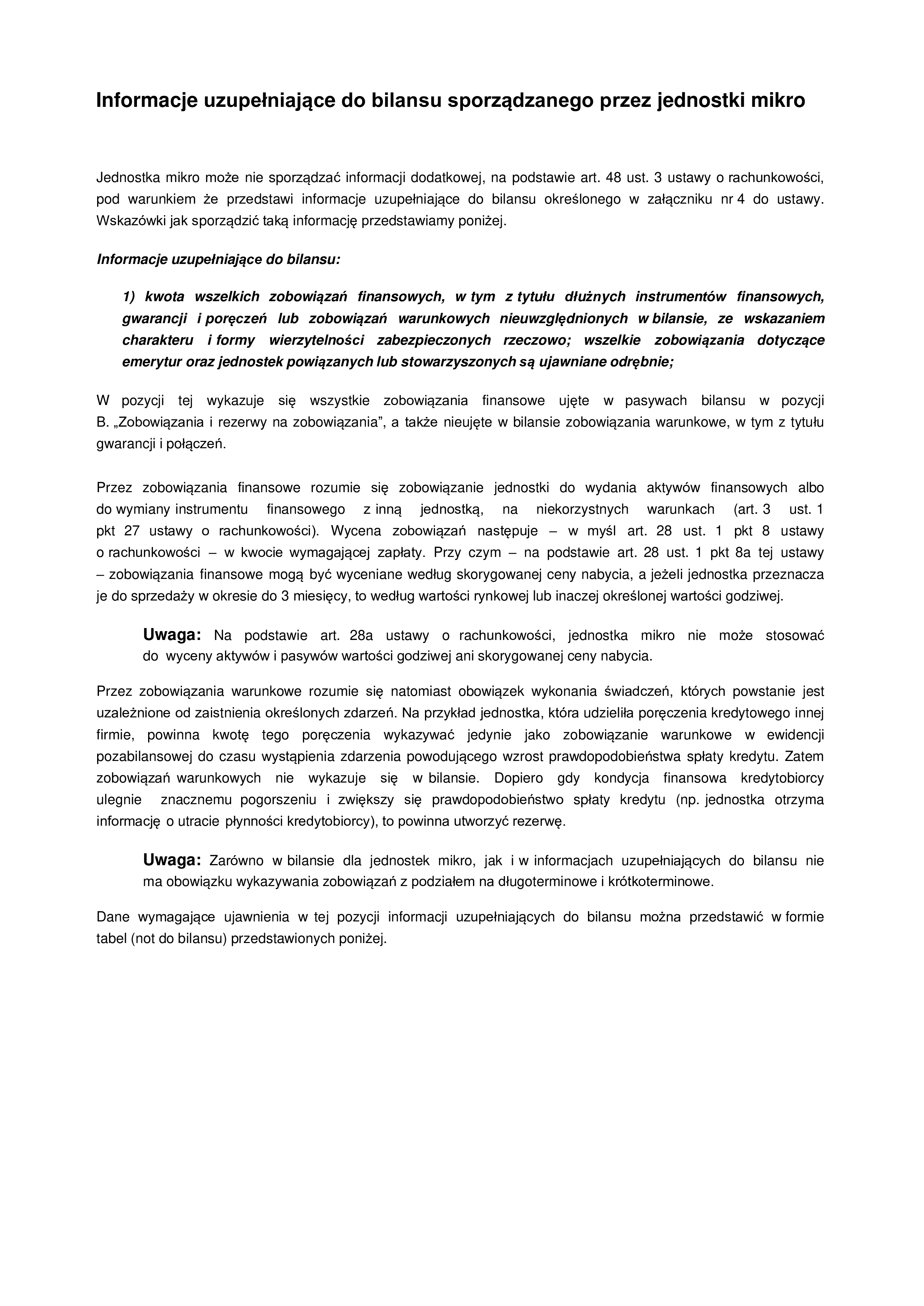

- Other Significant Information: This covers anything else that is relevant to understanding the financial statements but not already covered. This could include details of significant contracts, contingent liabilities, or events after the reporting period.

Example: Let's say your company has a significant amount of receivables. In the balance sheet, you'll see the total amount. But in the DII, you would provide a breakdown: "Trade receivables - PLN X, Receivables from tax authorities - PLN Y, Other receivables - PLN Z." This gives users a much clearer picture.

Or, if your company changed its depreciation method during the year, you must disclose this in the DII and explain the impact on the financial statements.

Why is the DII so important? Because it improves the transparency of the financial statements. It helps users – such as investors, creditors, and even the tax office – to make informed decisions. The DII ensures a complete and accurate understanding of the financial performance and position of the small entity.

In conclusion, preparing the Dodatkowe Informacje i Objaśnienia is not merely a formality. It's a vital part of the financial reporting process for small entities in Poland. Properly prepared DII enhance the credibility and usefulness of the financial statements, fostering trust and transparency.